Get a car quote now

Fill in your details below and we'll give you a call.

Get a car quote now

Insurance for your every need

Are you ready for royal service all the time, every time? Save with simple cheap insurance.

Insurance for your every need

Are you ready for royal service all the time, every time? Save with simple cheap insurance.

Personal insurance

From cars, to homes, to cellphones... Your stuff's safe in the king's capable hands.

Personal insurance

From cars, to homes, to cellphones... Your stuff's safe in the king's capable hands.

Learn more

Commercial insurance

Whether you're looking for business, engineering, community, or agri insurance... We've got your back.

Commercial insurance

Whether you're looking for business, engineering, community, or agri insurance... We've got your back.

Learn more

Life insurance

Life insurance, funeral cover, group schemes offerings... We've got it all.

Life insurance

Life insurance, funeral cover, group schemes offerings... We've got it all.

Learn more

Let's hear it for our royal family

Here's what some of our clients have to say about our simple cheap insurance products and royal service.

Let's hear it for our royal family

Here's what some of our clients have to say about our simple cheap insurance products and royal service.

“Joining King price insurance was the best decision I ever made when it’s come to choosing car insurance. The excellent service I have been receiving from King Price over the years is amazing. This company pride it’s self in ensuring customer satisfaction.”

Nomfundo M

5 Mar 2025 at 15:33 pm

“My claim was quickly processed and their service providers contacted me even before I got the affirmation from the insurance, I’m really satisfied and happy”

Elizabeth M

5 Mar 2025 at 21:47 pm

“The service is impeccable never had service like this, king price really takes care of their clients. Their response is amazing I will recommend to everyone and the staff are very friendly and kind”

Pragashni M

6 Mar 2025 at 08:33 am

“I was assisted by Kyle Bhawanipersad to switch my policy over to King Price. He was lovely and made a process that I was dreading a lot easier to navigate. He got me a good premium including everything I wanted covered and made the entire process easy to understand.”

Bianca H

26 Feb 2025 at 12:47

“Excellent Service provided by Anesu Ziramba. Frequent communication and update on progress of the claim. Excited about the friendly service I got😊😊👑thanks for the Royal Treatment👑🌹”

Dorah L

19 Feb 2025 at 17:57 pm

“I have had the best service interaction from Aaron Naidu at King Price Insurance! I was enquiring about getting possibly changing my insurance to save costs. I sent a request both on WhatsApp and email for assistance. I spoke to Aaron this morning, and was so surprised by the level of client interaction.”

Bernard

5 Mar 2025 at 17:34 pm

“I would like to write a review about King Price Insurance Thando Mavimbela is the best, I contact him for any changes to my policy. He is professional and always keeps his word. Wonderful service. Thank you.”

Stella

5 Mar 2025 at 17:11 pm

“I recently added another car to my policy. After a month I called them to check if they could assist with dropping high premiums seeing that I have more cars. They did not hesitate, they swiftly assisteed me. truly happy with the service and professionalism. Keep it up.”

Raphael M

5 Mar 2025 at 17:34 pm

“Kings Price - Gontse gave me the best service taking into consideration, being a pensioner & tough financial times in unstable economy. She was compassionate & fully understood our situation & made the policy that we need possible.”

Arlene G

26 Feb 2025 at 12:42 pm

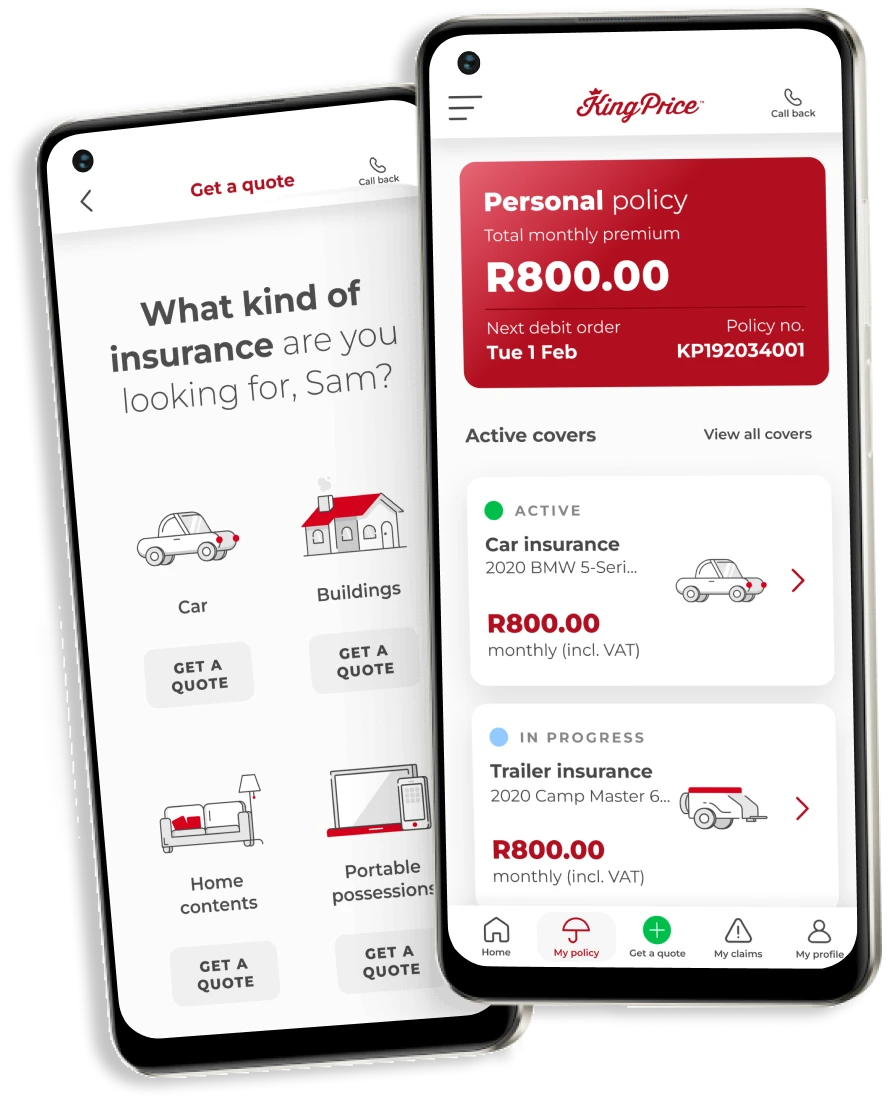

Manage your personal policy online

Manage your policy in just a few taps with our super handy self-service portal or app.

Manage your personal policy online

Manage your policy in just a few taps with our super handy self-service portal or app.

Frequently asked questions

Frequently asked questions

How can I get insurance from King Price?

King Price policies are sold online through our

self-service portal

or mobile

app.

You can also WhatsApp or call us on 0860 50 50 50.

How do I pay for King Price’s insurance?

Your King Price premium is payable every month, and must be paid in the way that you and King Price agreed upon.

What if I miss a premium payment?

If your premium payment doesn’t go through, you need to contact us. Remember, no premium paid = no cover.

What’s a policy renewal?

A policy renewal is the process of reviewing your existing insurance policy.

When do renewals take place?

The king’s renewals take place annually.

What’s an excess?

An excess is an amount you’ll pay towards a successful claim, and you can trust us to pay what’s due to you.

How does an excess work?

Let’s say you chose a basic excess of R5,000. After an accident, you claim from your insurer. The repairs cost R20,000. You’ll then pay R5,000, and your insurer will cover the rest (R15,000).

What number can I call in an emergency?

In case of an emergency, please call 0860 50 50 50 and listen to the prompts. You can also WhatsApp us on the same number if you need to.

What's an emergency?

We take emergencies very seriously, but what you might consider an emergency may not fall under the king’s idea of an emergency.

What are your personal insurance trading hours?

Mondays to Fridays

06:00 - 23:00 (online)

08:00 - 18:00 (client care)

08:00 - 17:00 (claims)

Saturdays

08:30 - 13:00 (claims and client care)

How do you keep my info private?

We highly value and respect your privacy (click

here

for our full privacy policy). We’ll never sell your info or share it with anyone except to provide our services and promote our business.

How can I get commercial insurance?

You can get a quote for our commercial products by filling in your details on our

website

(we’ll call you back ASAP) or by chatting to your broker. You can also give us a call on

1 of these numbers.

What’s dual insurance?

Dual insurance is when you have more than 1 insurance policy for the same thing. If you’ve insured an item with us and another insurer, we’ll only pay out our portion when you claim.

Am I covered for wear and tear?

Maintenance is up to you so that's a nope from us.

Couldn't find the answer to your question?

Don't worry, we're here to help you! You can either read through our full FAQs and if you're still not sure, you can

WhatsApp

or call us on

0860 50 50 50

.

Trusted and backed by the best

Some of the best insurers in the world have got our back...And yours.